Fashion

3 Fashion Stocks to Buy Before Summer 2024 Heats Up

Summer is around the corner, meaning fashion stocks are well-aligned. Sure, the “sell in May, and go away” stock market anomaly is worth considering. However, consumers will likely stock up on fashion items prior to their long-awaited summer holidays.

Seasonal consumer spending introduces a base case for better industry earnings. However, that doesn’t mean all fashion stocks are primed to surge. In fact, a comprehensive study is required to establish which, if any, fashion stocks are set to prosper in the coming months.

Methodologically, I screened for fashion stocks with telling fundamentals. Moreover, I ensured that each stock’s quantitative metrics were in order. Last but not least, I searched for overlooked intrinsic value.

With all that said, here are three retail stocks to consider ahead of the northern summer.

Nike (NKE)

Source: TY Lim / Shutterstock.com

Nike (NYSE:NKE) is a product launch play. According to Bank of America analyst Lorraine Hutchinson, the firm is set to reposition its product line ahead of the Olympics this fall.

Those factors play into broad-based summer spending, lending Nike the necessary latitude to benefit from seasonal sales. Furthermore, reports suggest that Nike is close to agreeing to an endorsement deal with Caitlin Clark, the Women’s National Basketball Association star. The agreement is reportedly worth $28 million and will span eight years. Although the Clark deal involves a substantial cost outlay, it enhances Nike’s footprint in the female activewear market, which is set to grow by 21.6% per annum until 2032. This is a good move by Nike!

Nike stock has slumped by more than 20% in the past year, placing its price-to-earnings ratio at around 27.69x, a five-year discount of approximately 33%. Although Nike stock’s poor performance raises concerns, I argue a value gap has emerged. Why? Well, Nike’s third-quarter earnings report conveyed fundamental prowess, as the company beat its revenue target by $130 million and its earnings-per-share (EPS) target by 23 cents. Nike’s fundamental resilience and aligned price multiples place its stock in undervalued territory. It means NKE stock is ready to provide its investors with stellar returns!

Lululemon Athletica (LULU)

Source: Sorbis / Shutterstock.com

Lululemon’s (NASDAQ:LULU) stock surged nearly 700% in the past 10 years, communicating the company’s fundamental stealth.

I believe Lululemon’s primary risk factor is its trend-like product line, which, although prominent, is niche. Secondly, LULU stock’s price-to-earnings ratio of about 29.88x is above the sector median of 17.38x, raising market-based doubts. However, despite these risks, I remain bullish.

Lululemon’s 10-year compound annual growth rate (CAGR) of 19.71% indicates secular growth. Moreover, Lululemon’s return on common equity ratio of 42.01% shows comprehensive monetization per unit of invested shareholder capital. These metrics speak volumes as they reflect perpetual growth.

Furthermore, Lululemon has near-term catalysts. For example, Brian Nagel of Oppenheimer recently said LULU stock’s growth prospects remain intact amid promising innovation and marketing. Moreover, as discussed in the introduction, fashion stocks could prosper before the northern summer, adding substance to LULU stock’s interim earnings prospects.

I highlighted LULU stock’s questionable price-to-earnings ratio earlier. However, I see this as both a momentum and growth play instead of a value stock. LULU’s illustrious growth rate will coalesce with systematic support in the fashion retail space to deliver unstoppable returns.

Guess (GES)

Source: Shutterstock

Guess’ (NYSE:GES) stock is filled with good news, which sent it above its 10-, 50-, 100-, and 200-day moving averages.

Even though some may deem Guess stock overbought, a sustainable growth story is in motion. The company walloped its earnings estimates last month after cruising past its revenue and EPS targets by $36.41 million and 44 cents, respectively. Moreover, Guess’ management approved a new share buyback program of up to $200 million, allowing the firm’s investors an opportunity to reduce their cost basis.

Furthermore, Guess and WHP Global agreed to acquire Rag & Bone. Guess’s $56.5 million commitment provides it full operating ownership and 50% intellectual property ownership. Rag & Bone delivered $250 million in revenue last year. Significant human capital and cross-border sales synergies are en route, providing Guess’ shareholders with much to cheer about.

Last, GES stock possesses a stunning price-to-earnings-growth (PEG) ratio of 0.2x, suggesting it is a growth-at-a-reasonable-price (GARP) investment opportunity. In my view, Guess’s PEG ratio coalesces with its robust fundamentals and momentum data points to formulate a bullish case!

On the date of publication, Steve Booyens did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

Antiques Roadshow guest’s daughter ‘scared to death’ by gambling wheel’s value

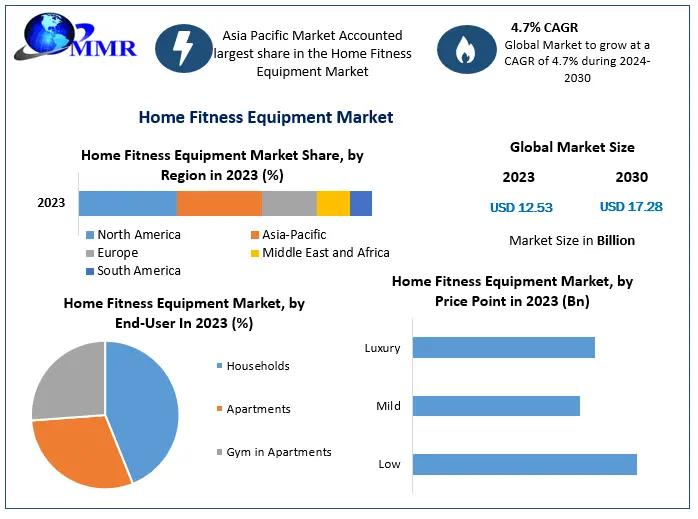

Home Fitness equipment Market Risk Factors, Economic Fluctuations, Drivers in Future Analysis by 2030

The Very Group launches Haus of Flamingo fashion platform, developed in collaboration with The Gate — Retail Technology Innovation Hub

CSI Softball seeking berth to NJCAA World Series

Tesla cuts all but 3 of its 3,400 listed jobs in North America

Dada meets dresses: why clothes that look like sculptures are all the rage

Does walking really count as a workout? Here’s what an expert trainer says

Fitness Equipment Market Is Expected to Exhibit Significant Growth Over 2031 Anta Sports Products, Ltd., Core Health & Fitness LLC, Icon Health & Fitness, Inc., Impulse Health Technology Co., Ltd.

Japan’s Olympic medalist and world champion Shoma Uno says he’s retiring from figure skating